THE INFLATION BLAME GAME AND MARX'S CRISIS THEORY

- Mike Treen

Inflation is back worldwide, and with it is the blame game. So, what is the truth behind the claims and counter claims that are being made? First, a little background. An impending worldwide recession in late 2019, foreshadowed by a freeze in the US repo* markets, led the US Federal Reserve to embark on a major amount of money printing. Interest rates were pushed down to free up credit. *A repurchase agreement, also known as a repo, RP, or sale and repurchase agreement, is a form of short-term borrowing, mainly in Government securities. Wikipedia.

In early 2022, public health measures -- economic closedowns -- imposed in response to the covid-19 pandemic further disrupted world production and trade. Both money printing by central banks across the globe and Government budget deficits were massively expanded to cope. Interest rates were driven below zero in some cases. People were actually being paid to borrow money - imagine that.

The monopolies dominating global production and trade also seized on genuine or manipulated shortages to impose price gouging wherever they could. The profits of energy companies, for example, simply exploded as a consequence. Most central banks, including the Reserve Bank of New Zealand, ignored the growing inflation and sought to blame the temporary supply chain disruption for the price increases.

Rightwing economic and political voices schooled in the "monetarist" schools of thought, which say inflation is always a monetary phenomenon (although none of them agree on what money is), stayed silent. They sensed that their system had dodged the bullet of a broader economic collapse. The extraordinary explosion in the global asset wealth of the ruling class that kicked in over late 2020 and through 2021 was also a factor in muting criticism, I'm sure.

But the monetarists were allegedly in charge of economic and monetary policy in 2008 when the US Federal Reserve started the process of money printing, dubbed "quantitative easing," for the first time around to get out of the deepest crisis of world capitalism since the 1930s' Great Depression. They had ignored their theories to save their system then. It seemed to work that time without triggering broader inflation other than in their assets, so maybe it would also work this time.

But today, we have inflation averaging 9-10% over much of the globe. These are numbers not seen for decades. Turkey, Argentina, and Sri Lanka have inflation rates of 60-80%. There is now a risk that continuing current policies will unleash hyperinflation of the US dollar in particular, which will destroy its value and end its role as the dominant world currency. From the point of view of the 1% owners of the world's wealth, that must be prevented at all costs.

Hyperinflation was threatened once before in the late 1970s when US inflation hit 13%, and there was a flight from the dollar into gold which doubled in value over a few months in late 1979. This required what was dubbed the "Volker Shock" in the name of the then US Federal Reserve Director Paul Volker, who stopped "easing" the monetary expansion and restored confidence in the dollar by pushing the Fed's official interest rate up to 20%.

Government spending on welfare and education was also targeted for cuts. "Austerity budgets" became the norm. Aiming for a budget surplus became economic orthodoxy across the major capitalist nations, although this was only achieved temporarily in the US, given the demands of its permanent wars of empire across the globe. After the inflationary 1970s in New Zealand, we had our version of the Volker Shock under the new Labour government elected in 1984, and the official interest rate reached an all-time high in 1985 of 18%. Variable mortgage rates hit 20%.

Financialisation And Deindustrialisation

Of course, capitalists who were in the business of lending money rather than producing goods were massively advantaged by high interest rates. There is also no reason to open a business unless the profit rate is above the cost of money. Marx explained in "Capital" that a capitalist will never invest in new production unless the profit of enterprise is above the rate of interest and, therefore, able to generate at least the average rate of profit. That is the economic origin of financialisation and de-industrialisation in the advanced capitalist countries as, literally, General Electric became GE Capital.

The 1% don't care how they make their money. But accumulated wealth needs to be stored in both financial and non-financial assets. Historically this was broadly a 50/50 share, but a gap has opened in favour of financial assets since 2008. The 1% hate inflation with a passion as it reduces their financial asset values by that percentage or more. Working people also get angry at price increases and may join protests and strikes to protect their living standards. And, in normal circumstances, central banks will move to raise interest rates and slow the economy to stop it. This will, at least temporarily, hurt profits and share market prices.

But in 2008 and 2020, central banks tried to keep the economy from contracting further than it already had (in 2008) or was expected to do (in 2020) by printing money through what is known as "quantitative easing". In 2008 this did not lead to much inflation as the recession had already hit hard in the US, so the money was hoarded by the 1% or used to settle debts among themselves rather than boost spending more broadly. But the latest round of quantitative easing involved both central bank money printing and Government budget deficits to save the system. The money was also given to ordinary people to spend. Inflation was inevitable.

It is the owners of wealth that determine central bank and Government policies on these matters, and the war on inflation will continue for as long as necessary and justified as essential for a nation's economic survival. For the Rightwing politicians and their economic "thinkers" dubbed monetarists, economists have rediscovered their orthodoxy and say the fault lies with too much Government spending and too much central bank money printing. Unfortunately, they are correct to an extent, but without fully understanding why. The question they need to be asked is why they stayed silent when it was happening.

Budget Deficits As A Cause Of Inflation

In the 1970s, the principal means of creating money and fuelling inflation was to run budget deficits. The US also needed to do this to finance the war in Vietnam. The economic orthodoxy at that time became known as Keynesianism after the UK economist John Maynard Keynes. Keynes was an upper-class, classical, pro-capitalist, free-market economist but accepted something must be wrong with the classical view when the economic depression that couldn't happen under those theories did happen in the 1930s.

He came to the view that the economy may need the assistance of lower interest rates from central banks or a budget deficit at times to stimulate demand and employment. Robert Muldoon in New Zealand, Prime Minister and Minister of Finance from 1975 to 1984, and US President Richard Nixon (1969-1974) were public supporters of Keynesian policies despite their Rightwing politics. Keynes also was not a friend of workers. He thought the cure for inflation was to cut wages through wage controls.

However, in the period after World War Two, budget deficits became endemic. The end result was dubbed "stagflation," a combination of inflation and economic stagnation. This is the worst of both worlds for working people because wages are cut by inflation while our ability to resist is undermined by high unemployment. That is why socialists don't favour Keynesian policies over monetarist policies. It's the capitalist system and its inevitable crises that is the problem, not the policies designed to manage the crises.

The Keynesians were removed from operational control and replaced by adherents of the monetarist school. The principal theorists of monetarism were from the University of Chicago School of Economics, led by Milton Friedman. As well as allegedly wanting to control inflation, they were also radical free-market dogmatists who favoured austerity for workers, free trade in goods, free movement for capital, free interest rates, and the privatisation of everything, including education and health care. They also support eliminating the minimum wage and unions because these "interfere with the market". The Act Party in New Zealand is an adherent of this school. They favoured tax cuts for the rich and regressive consumption taxes on us.

With monetarists in charge, budget deficit financing was sharply curtailed - especially on spending that assisted working people - like welfare, health, and education. Infrastructure spending was starved. Central banks like New Zealand were made "independent" with the exclusive goal of targeting inflation to keep it low. Money supply was to be controlled through interest rate increases each time the economy started growing a little and unemployment began falling. Conveniently for the Rightwing political leaders, their theories are also deeply anti-working class.

The Chicago Boys were invited to Chile to transform the economy in favour of the rich under the military dictatorship of General Augusto Pinochet after he seized power from a socialist-minded Government in a coup in 1973. A Slate magazine report from January 12, 2016, headed "The Boys Who Got To Remake The Economy" explains the policies of the people put in charge of the economy:

"Their programme centred on reductions to fiscal spending to solve high inflation and economic difficulties. They opened the economy to foreign imports, privatised dozens of State companies, and removed most Government controls on private economic activity. At the same time, as it was opening up the Chilean economy, the regime was clamping down on political opposition. In Pinochet's nearly 20 years in power, thousands of people were killed or 'disappeared'".

"But while it came under heavy human rights criticism, Chile was the first country to apply Friedman's economic principles, and, years later, the famous economist called this process, led by his disciples, "the Miracle of Chile." Friedman himself visited Chile and met with Pinochet in 1975, where he praised the economic measures taken by the Chicago Boys and Pinochet's government. The connection with the dictator has been one of the most controversial aspects of Friedman's legacy in the United States". The UK followed Chile's policies under Prime Minister Margaret Thatcher in 1979, the US under President Ronald Reagan in 1981 and New Zealand in 1984 led by a Labour government Finance Minister and future Act Party leader, Roger Douglas.

Neoliberalism Triumphant

These policies were dubbed "neoliberalism" to mark them out from the previous Keynesianism. It was theoretically possible for a Government to stop the budget deficits and fight their inflationary impact by taxing the rich or eliminating war budgets. No capitalist Government from that time tried to do that, of course. Adherents of monetarism and its free-market dogmas were put in charge of every aspect of Government policy.

For example, that is why the economists at the New Zealand Government agency responsible for the labour market policies - the Ministry of Business Innovation and Employment (MBIE) - predict every year that the proposed rise in the minimum wage will lead to more unemployment when the opposite has happened year after year.

The monetary side of these policies was abandoned almost overnight when the 2008 crisis hit. This was considered necessary to stop a system-wide collapse of the banking and financial system in the US and Europe. All forms of debt exploded across the globe, but this was seen as the price of the rescue of the private profit-seeking system. But then the recovery of world capitalism following that was the slowest in the history of capitalism. It was becoming clear that the world was gearing up for a renewed slowdown in late 2019, and then the pandemic hit.

The capitalist rulers knew they needed new doses of money printing and Government spending to save their system. Capitalists only produce if they can sell goods for a profit. They only lend money if they feel they will get their money back with interest. Essentially the State in almost every country has stepped in to protect those profits whenever they get threatened.

A central bank can create money by simply printing it electronically. What that gets used for, however, is something that can be different in different periods. During the most recent crisis, the US used the money to buy up bonds from distressed banks and industrial corporations to prevent them from going under. In New Zealand, $28 billion was given virtually free to the banks to lend directly to whoever they wanted. They gave most of it to property speculators who drove up house prices by 30% in one year. Another $100 billion was made available to the Government to prop up businesses during the pandemic.

This allows the Government to run big budget deficits without horrendous interest rates being demanded (at least initially) by the private financial capitalists for the bonds they issue to finance the debt. This is "unorthodox" by any measure but was considered necessary by everyone as the crisis hit. Now we are being told that the Central Banks will be returning to more orthodox policies over the medium turn.

The return to orthodoxy means the central bank must retire the bonds that it has created by buying them back, and they need to push up interest rates to do so. But, in the absence of taxes on wealth, the budget deficits are also being targeted because they create spending artificially - a form of money creation but different from the central banks printing money directly. Reducing these deficits will be contractionary for the economy.

This will inevitably induce a recession in New Zealand over the next year or so. This is also true for Europe and the US, and the whole globe. The cost of the rescue of the capitalist profit-seeking system will now be unloaded on working people because the crisis that is coming has been made that much bigger and more dangerous by the escalating debt levels.

World Capitalism Got Out Of The 2008 & 2020 Crises With Massive Debt Creation

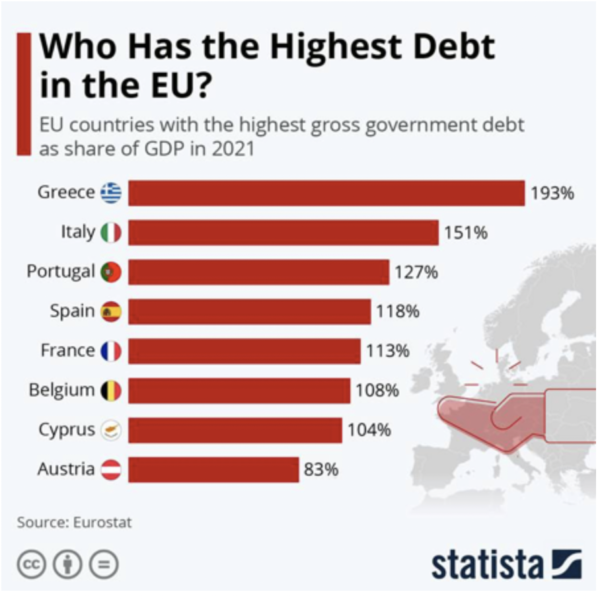

The US public debt is the most important indicator of this process because of the weight of the US economy. From about 60% of gross domestic product (GDP) before the 2008 crisis, it exceeded 130% after the 2020 recession. In the European Union (EU), the average debt-to-GDP ratio was 88% at the end of 2021. Although the EU's founding Maastricht Treaty provides for a maximum of 60%, many countries are well above the 100% of GDP level, as the table shows

On a global level, according to the International Monetary Fund, "Global debt (public and private) rose by 28 percentage points, to 256% of GDP, in 2020 (i.e., in the course of one year) ... The global public debt ratio jumped to a record 99% of global GDP".

Global debt is now 256% of global GDP. At the end of World War Two, after the massive borrowing to pay for the war, it was around 100%. It remained around that level until the end of the 1970s. Besides acting as a break in terms of fiscal policy, this avalanche of debt, coupled with rising interest rates, will definitely push a number of economies towards default. This applies to some heavily indebted rich countries like Greece and Italy but will savage many poor countries.

The debt problem is not only affecting states but also corporations. Morgan Stanley calculates that 16% of US firms are "zombies" (highly indebted companies hanging by a thread). Bloomberg reports that zombie company debts total $US900 billion. This is not only a US phenomenon. Zombies account for more than 20% of Europe's companies, according to DW.

High-interest rates (meaning the end of the "cheap money" era) will make it much more difficult for these companies to re-finance their debts, which can lead to defaults - which in turn means mass layoffs of workers. The world is also being hit by a double whammy of war-induced shortages and price rises for basic food, fertiliser, and other commodities. This will accentuate the downturn.

The US currency is rising against most others because there is a flight of capital to the safety of the world's biggest and safest financial market. This means the poor countries' debt, usually in US dollars, is getting increasingly unpayable. As Oxfam notes in a new analysis, during the pandemic's second year (from March 2021 to March 2022), the International Monetary Fund (IMF) approved 23 loans to 22 countries in the Global South - all of which either encouraged or required austerity measures.

Global Poverty Accelerating

The International Monetary Fund has announced that the global economy is entering a major slowdown, downgrading the growth prospects of 143 countries. At the same time, inflation rates have reached historic levels. Around the world, hundreds of millions of people are falling into poverty, particularly in the Global South. Oxfam has sounded the alarm that we are "witnessing the most profound collapse of humanity into extreme poverty and suffering in memory".

David Beasley, the Director of the UN World Food Programme describes the situation in the following terms:

"Even before the Ukraine crisis, we were facing an unprecedented global food crisis ... Then, we thought it couldn't get any worse, but this war has been devastating". He added: "...the number of people suffering from 'chronic hunger' had risen from 650 million to 810 million in the past five years... the number of people experiencing 'shock hunger' had increased from 80 million to 325 million over the same period. They are classified as living in crisis levels of food insecurity, a term he described as 'marching towards starvation and you don't know where your next meal is coming from'...".

"... 'after the economic crash of 2007-09, riots and other unrest erupted in 48 countries around the world as commodity prices and inflation rose… The economic factors we have today are much worse than those we saw 15 years ago'. If the crisis was not addressed, he said, it would result in: 'famine, destabilisation of nations and mass migration'".

And concluded: "It is a very, very frightening time. We are facing hell on earth if we do not respond immediately". But the World Bank and IMF solutions for the crisis these nations face are more free market and privatisation policies. This is what is now being imposed on bankrupt Sri Lanka as the price of a bailout from bankruptcy. It is the price the Zelenksy regime in Ukraine has agreed to pay for NATO support against Russia. The climate crisis is also being compounded because the capitalist crises and imperialist wars are driving up the production of planet-destroying energy sources. Capitalists have no alternative but to be capitalists, and the planet is doomed if we continue business as usual.

Covid-Aftermath Boom

The cause of the current crisis is the overproduction of commodities in the covid-aftermath boom. Capitalists were cautious about accumulating inventories and investing after the 2007-09 bank crisis and the Great Recession. This prevented a new worldwide overproduction crisis for some years at the price of lingering unemployment and eroding living standards. Stagnation appeared to be the new norm. However, by late 2019 signs of overproduction were again developing, causing a spike in interest rates, though the situation had not yet reached a crisis.

But then came covid. In March 2020 the ruling class feared the virus would decimate the working-class population to such an extent their ability to squeeze surplus value out of the survivors would be impaired. They used State power to shut down much of the economy, throwing millions out of work overnight. The covid shutdowns also caused a forced underproduction of commodities and reduction of inventories.

When the shutdowns were eased, the boom began to rebuild inventories as demand for commodities soared. Demand exceeded supply at prevailing prices, resulting in high prices and higher profits. There was a rise in demand for labour power. But wages didn't keep up with inflation, so real wages declined. The Critique of Crisis Theory blog highlighted the accelerating signs of crisis in a post on May 22 (2023) headed: "The Phony Crisis, The Real Crisis, And The Whip Of Hunger".

"The massive overproduction resulting from the covid aftermath boom has pushed the economy to the brink of what could become a deep recession. This is shown by the collapse of four regional banks, as well as by leading indicators such as the relationship between short-and long-term interest rates, called the yield curve - and measures of the money supply, dollar bills, coins, and bank deposits, that function as currency. The yield curve has not been so inverted - short-term interest higher than long-term - since the early 1980s. The global money supply, a predictor of approaching recession, has also been contracting at rates not seen since the super-crisis of the early 1930s".

"If this was not enough, the dollar price of gold has been above $US2,000 for several weeks as I write these lines on May 13, 2023. Its significance is that if the Federal Reserve System tries to stave off the crisis by moving to reverse the contraction of the global money supply, a run on the dollar could develop that has the potential to sink the dollar-denominated international monetary system, the financial foundation of the US empire. Many countries have already built up gold reserves and taken other steps to reduce their dependence on the dollar".

Whenever a global crisis of the overproduction of commodities approaches, Governments come under pressure to limit their borrowing and spending. When plenty of money and credit is available, central Governments can borrow without reducing the quantity of loan money available to the rest of the economy. But when loan money starts to dry up, as it does just before a recession, Government borrowing accelerates the credit crunch in the economy".

There is much discussion today around how effective monetary policies are in regulating the ups and downs of the business cycle. Monetary policies are run by the central banks, with the US Federal Reserve operating like the world's central bank. Their principal tools are setting certain interest rates they can control or influence and creating or reducing the supply of token money.

Law Of Value Operates Through The "Invisible Hand"

There are laws that capitalism must obey. The first great economic thinkers associated with the birth of this system were Adam Smith and David Ricardo. They explained how the system worked. Smith coined the term of the "invisible hand". As the pro-capitalist site Investopedia explains: "The invisible hand is a metaphor for the unseen forces that move the free market economy. Through individual self-interest and freedom of production as well as consumption, the best interests of society, as a whole, are fulfilled. The constant interplay of individual pressures on market supply and demand causes the natural movement of prices and the flow of trade".

This invisible hand is based on the law of labour value that Smith and Ricardo both accepted and that Karl Marx incorporated into his writings and took to their final, most scientifically developed form. Marx showed in "Capital" that prices (exchange values) are the form that labour values take. But, as always, there's a contradiction between appearance and essence. Aggregate market prices can diverge from aggregate labour values (or at least what they would be if they accurately represented labour values). During a boom, prices drift above values.

Marx corrected the classical labour theory of value to show that a commodity's price did not oscillate around a "natural price" based upon actual labour time, but around a "price of production" that took account of the ratio of labour and capital relative to the average, and the turnover time. An individual commodity goes to the market to see what claim it can make on society's finite amount of labour time. In total, aggregate values equal aggregate production prices. However, the credit system divorces the act of purchase from the act of paying.

Lenders can lend more than they have - they leverage. This pushes up aggregate market prices above their respective countries' labour values. Claims are being made on future labour time that may never be realised. In a boom, everything appears to be going swell, and leverage continues to increase until the "Minsky Moment" - a sudden collapse in value and some lenders start to panic that they may not get their money back.

We then get credit crunch, financial crisis, and recession. The law of value acts. Marx's theory, contrary to myth, fully integrates the market, as the value of a commodity cannot be known until it comes to the market. That is, it isn't the actual amount of labour time inherent in the commodity that gives it value, rather the amount of society's finite labour time it can claim in the marketplace.

Before fiat money, the capital devaluation was obvious in price deflation. With fiat money, we get currency devaluation, as in the 1970s, 2008, and again today. In all three periods, currency prices in gold rocketed. In "gold price" terms there was deflation. And the reason gold still features in financial markets because it takes a certain amount of labour time to produce an ounce of it. It is still a measure of value, as distorted as it may be due to speculation.

Three Types Of Money In Existence - Gold, Credit Money And Token Money

To understand what is happening we need to understand the interaction of three types of money in existence today. One form is gold which as a product of human labour has emerged as the universal equivalent of all other commodities as a measure of value. All societies with a developed system of commodity production and exchange need a universal equivalent to function. Gold can also be hoarded for its intrinsic value, especially in times of monetary disorder. Gold does not disappear. It always retains its value through any crisis. Capitalists and central banks hold a portion of their wealth or reserves in gold because of these special properties.

The second form of money is token money issued by the State, dubbed "fiat" money by economists. So long as the currency is not "over-issued" relative to the existing quantity of gold, the currency - whether it be dollars, pounds, yen, or rupees - can retain its value so long as it is backed up by a State power which can impose taxes and use force on those it wants to do its bidding.

But if the currencies are "over-issued,"" they lose value in proportion to the over-issue. In normal circumstances, a doubling of token currency will result in a halving of its individual value. In other words, the currency price of gold will double. This is the origin of general price inflation we saw during the 1970s and early 1980s. Then US President Richard Nixon declared "we are all Keynesians now" and believed he could finance the Vietnam War without massive cutbacks in social spending in the US through budget deficit spending. The end result was a steady devaluation of the US and other currencies and endemic inflation worldwide.

The first casualty of this policy was for the US dollar to cut its link to gold at $US35 an ounce in 1971. They claimed they would then be "free" of the gold "shackle" as it was dubbed by opponents of the gold standard. However, being free of the shackle only encouraged further devaluation. The price of gold hit $US120 an ounce in 1976. Soon we had "stagflation" - inflation and economic stagnation at the same time. By the late 1970s, there was a flight out of the US dollar into gold that saw the "price" of gold soar to nearly $US600 an ounce.

To prevent a total collapse of the currency, the US Federal Reserve had to stop further accelerating the rate of growth of the dollar it created, which, in turn, boosted interest rates to record levels of 20% for the Federal Funds Rate and drove the country into a deep recession. Bad as inflation was - especially for real wages of the working class, which was being paid in debased currency - from the viewpoint of the capitalist economy the worst result was this rise in the rate of interest. Inflation dropped from 14.8% in March 1980 to 3% by 1983. By the mid-1990s gold stabilised for a period at around $US400 an ounce.

The amount of token money that can be issued is governed by the total amount of gold bullion in existence in the world. This usually expands at a relatively steady pace of, say, 2% a year, so it is a relatively safe bet that token money can also be increased proportionately. But gold production also has its own cycle which runs counter to the normal industrial cycle and impacts interest rates and places objective limits on token money and credit creation. If there were no objective limits to the creation of token and credit money there would never be a crisis of generalised overproduction every ten years or so like we have seen throughout the 150-year history of developed capitalism.

These crises have been analysed and explained by Karl Marx as being generalised crises of overproduction relative to the ability of the market to absorb these commodities at prices that guarantee the producer at least the average rate of profit. Overproduction is reflected in growing inventories, factory shutdowns, and unemployed workers. If token money or credit could be expanded at will forever, then there could be no such crises. That is why pro-capitalist economic writers can't explain why they happen.

Monetarists don't understand the different forms of money. They treat gold, credit money, and token money as essentially the same. Keynesians also don't understand the different forms of money and why gold retains its essential role as a measure of value in economic life. Both Keynes and Friedman predicted that the price of gold would collapse once the State was stopped from being able to exchange their currencies at a fixed rate to gold. Of course, the opposite has happened, as Marx predicted it would.

Monetary authorities don't really understand the exact total of token money they can issue without devaluation. They operate to a great degree on trial and error. They don't know what they are measuring the currency against, but the consequences of over-issuing become apparent very quickly in a rising price of gold, a broader leap in commodity prices in terms of the devalued currency and then a general rise in prices. This forces the central bank to increase interest rates, cut back on the currency being issued, or purchasing previously issued currency to neutralise it. Failure to take action can lead in some extreme circumstances to hyperinflation and a currency collapse.

The third form of money is credit money. Under a developed system of finance and credit, this credit money is created and centralised by the banks through making loans. They are able to use deposits of token money created by the central bank as a base from which to expand lending many times over the actual sums deposited amounts of customer deposits. So long as everyone doesn't want their money back at the same time the merry-go-round can continue. This is called fractional reserve banking.

But banks are profit-making competitive businesses. They have a built-in tendency to seek more and more creative ways to create and extend credit to maximise their returns. Derivatives that serve as a kind of insurance against loans going bad are the latest example of that. Eventually, as inventories of unsold commodities pile up and credit tightens a breakdown happens, which will begin at the weakest links of the credit chain. A credit crisis and collapse of at least the most over-extended institutions then follows. Credit money is not "real" money like gold and can disappear completely without a trace. In fact, the over-issuance of credit must be periodically neutralised for the system to restore balance.

If there is no reduction in credit money then it is essentially being converted into token money. This will fuel an inflationary surge sooner rather than later with the inevitable consequences of a spike in interest rates leading to a deeper credit contraction, the very thing that conversion of credit money into token money is designed to avoid. In the current crisis, the Federal Reserve is forced to prop up bank deposits as the currency system is threatened on one side while staving off the collapse of the dollar-centred international monetary system on the other. These are contradictory goals.

Crises Bring Values And Prices Into Line

The point of capitalism's recurrent crises is to bring aggregate market prices back into line with aggregate values. Before a crisis hits, prices have inevitably been inflated by leverage. Before 1971, crises took the form of price deflation. Since the decoupling from gold, currency prices can increase, but capital still gets devalued in terms of "gold prices" as the currency itself depreciates. The 2007/08 debt deleveraging was short-lived, as the ruling class bailed itself out and passed austerity onto everyone else. The debt bubble and the discrepancy between aggregate market prices and aggregate values, however, remained and grew.

Pro-capitalist economists can't understand capitalism's recurrent crises when they have the wrong, subjective, marginalist theory of value. Price and value are always equal in marginalist theory. With the wrong theory of value (marginalism), you have the wrong theory of prices; the wrong theory of money, and you can't even build an objective theory of the business cycle (hence Keynesians blame the "poor animal spirits" and monetarists blame central bank mismanagement).

The operation of the law of value under capitalism led to industrial cycles of boom and bust that ultimately produced a larger and more powerful system of production that conquered the globe. The system would rebound more strongly during periods of recovery if the laws of motion governing that system are allowed to do their magic. That continued to be true after World War 2 for two for three decades because of the depth of the Great Depression and the suppressed demand for consumer goods as a consequence of the War itself.

With Marx's theory of value (not the same as the classical labour theory of value), you have an objective theory of the business cycle based upon the excessive creation of credit money leveraging aggregate prices above their value equivalent (the market extended by debt), that results eventually in a credit-crunch, financial crisis & recession.

Prices Get Brought Back In Line With Their Value Equivalent

When there was a gold standard, that meant deflation followed inflation. Now currencies (token money) get devalued (as measured by gold). Thus, the stagflationary 70s still saw prices fall as measured by weights of gold. Since 1987 central banks have reflated the bubble with more token money. We now have the biggest distortion from values in capitalism's history. Bringing this back to balance will most likely require another Great Depression. The scale of the rescue operations has become staggering. This Financial Times report reprinted in the NZ Herald (31/1/23) notes:

"Since 1980, the US economy has spent only 10% of the time in a recession, compared with nearly 20% between the end of the Second World War in 1945 and 1980, and more than 40% between 1870 and 1945. One increasingly important reason is Government rescues. Combined stimulus in the US, the EU, Japan and the UK, including Government spending and central bank asset purchases, rose from 1% of gross domestic product in the recessions of 1980 and 1990 to 3% in 2001, 12% in 2008 and a staggering 35% in 2020".

Both the Keynesians and the monetarists have attempted to stop the law of value from operating with full force by using fiscal or monetary policies to stop a deep recession happening that would clean out the least productive capitalists (industrial or financial) and reward the most efficient and productive capitalists. The only results possible by these policies have been either an inflationary crisis or an explosion of debt that can never be repaid. Today, protecting that debt from the operation of the market to reveal its true value drags the entire system toward permanent stagnation and depression.

Financialisation

The crisis has been accentuated by the financialisation of economic activity over the last three decades following the Volker Shock. This has created a tiny financial oligarchy that controls most economic activity on the globe. Financialisation was also associated with an explosion of all forms of debt - personal, Government, and corporate debt. But rather than this debt being used to accelerate growth under capitalism, the greed and predations of the dominant financial oligarchy appear to have become a brake on the system. Growth over each of the last three decade-long cycles has been progressively weaker despite (or maybe because of) the ever-growing debt.

But this financial oligarchy calls the shots on what type of Government policies are considered acceptable. The debt market and interest rates are used to police those Governments when necessary. This is especially true when it comes to monetary policy. After the inflationary 1970s it was an article of faith that no Government would be allowed to simply print money and spend it - especially on social programmes that benefited working people. Tax cuts for the rich were OK because that caused the Governments to be even less able to spend money on anything useful.

Central banks were removed from Government control and made "independent" to prevent inflation beyond 2-3%. Many Governments, including both Labour and National in New Zealand, turned the need to always run budget surpluses into a religious dogma. All those dogmas have now been abandoned without explanation. Pushing back against complaints about their policies, the Reserve Bank Governor Adrian Orr simply asserted that booming house prices were a "first-class problem" and that the alternative is "recession or depression" (13/11/20). That may be true, but we have a right to discuss alternatives to how the money being created should be used.

Essentially the world has gone through two crises over the last few decades where it became necessary to print money on a vast scale and simply hand it to the 1% who control the banks and other financial institutions to use to facilitate payments between themselves. No alternative policies have been allowed by the "independent" Reserve Banks and Governments serving the 1%.

The following warning from Nouriele Roubini shouldn't be dismissed out of hand: "For now, loose monetary and fiscal policies will continue to fuel asset and credit bubbles, propelling a slow-motion train wreck. The warning signs are already apparent in today's high price-to-earnings ratios, low equity risk premia, inflated housing and tech assets, and the irrational exuberance surrounding special purpose acquisition companies, the crypto sector, high-yield corporate debt, collateralised loan obligations, private equity, meme stocks, and runaway retail day trading. At some point, this boom will culminate in a Minsky Moment (a sudden loss of confidence), and tighter monetary policies will trigger a bust and crash" (2/7/21).

The Federal Reserve System faces a quandary: If it creates more dollars not backed by gold to keep the boom going, profits in dollar terms would remain high for a while but turn negative in gold terms. This would cause capitalists to transform as much of their capital as possible into gold. The resulting run to gold would accelerate dollar inflation and threaten to bring down the dollar-centred international monetary system.

On the other hand, if the Federal Reserve allows the bank money system to become paralysed by bank runs, the dollar would be saved, but the economy would fall into a second Great Depression. So, the Federal Reserve is attempting a middle way: to keep the system of bank deposits as currency functioning, without bringing down the dollar's role as the world currency - and other currencies linked to it.

The aim is to achieve a relatively soft landing, even if that means a recession with millions losing their jobs. But if the Federal Reserve is successful, it will keep a recession from turning into a depression, while saving the international monetary system. Whether the Federal Reserve can pull it off this time remains to be seen. But even if it does, the world will face a similar crisis again in a decade or so.

Huge Growth In Inequality

The direct consequence of handing the financial oligarchy trillions of dollars in the midst of one of the worst economic crises in human history is that the 1% has hugely expanded its wealth and power with inflated asset prices, and stock market values over the past years. Michael Roberts reports: "The top 1% of households globally own 43% of all personal wealth while the bottom 50% have only 1%".

"The 1% are all millionaires in net wealth (after debt) and there are 52m of them. Within this 1%, there are 175,000 ultra-wealthy people with over $50m in net wealth - that's a minuscule number of people (less than 0.1%) owning 25% of the world's wealth!". Working people across the globe are caught in a dilemma. We don't want an economic collapse because we know we will be the worst affected. So, actions by Governments to "rescue" the entire capitalist system of finance and production and trade are needed.

But if we are going to do that, why don't we place the commanding heights of the economy, especially in the area of finance and money creation, into the hands of a publicly-owned and democratically controlled entity rather than simply hand the 1% our cash as if they have some God-given right to it? We have socialised all risk associated with private banking, so why not socialise banking itself? We must now build for a future that involves putting people and the planet before the pursuit of private profit.

The current combination of policies to combat the pandemic and associated economic crisis - which involves both a monetary and fiscal explosion - will sooner or later lead to an implosion of the entire credit and monetary system and along with it the system of capitalist production itself. The alternative is not to let capitalism operate without any limits in terms of subjecting all labour and the planet to its uncontrolled passion to exploit all and everything for the private benefit of a tiny class of owners. The planet cannot survive another few decades of the same old shit.

Working people need to put forward solutions in the here and now that protect our class and the planet we live on in an immediate sense. Those immediate demands can form part of a programme to transform the way we produce and live with each other. But we should do so with our eyes open to the fact that this system cannot accommodate what we need without generating new forms of crises.

The creation of money, in all its forms, should be a publicly controlled process without capitalist greed periodically putting entire financial systems at risk and that we end up having to bail them out because of their greed and that they are "too big to fail". This is effectively what happened in Ireland, the UK and US after the 2008 crisis and we should make sure we do not repeat this time as we face the economic dangers ahead.

We must be prepared to go beyond a system based on private greed towards one based on human needs - a socialist world. The economic struggle against capitalism and for socialism isn't about distribution, it's about the private ownership of capitalist production. In the "Critique Of The Gotha Program" Marx says that capitalist distribution stems directly from capitalist production: "Any distribution whatever of the means of consumption is only a consequence of the distribution of the conditions of production themselves. The latter distribution, however, is a feature of the mode of production itself".

Marx then says that the hardship that the workers face from capitalist distribution (i.e., the outrageous price of goods and services, the impoverishment of the unemployed, and so on) is because of the private ownership of capitalist production: "The latter distribution, however, is a feature of the mode of production itself. The capitalist mode of production, for example, rests on the fact that the material conditions of production are in the hands of nonworkers in the form of property in capital and land, while the masses are only owners of the personal condition of production, of labour power".

"If the elements of production are so distributed, then the present-day distribution of the means of consumption results automatically". Then he writes the solution to this that: "If the material conditions of production are the cooperative property of the workers themselves, then there likewise results a distribution of the means of consumption different from the present one".

Marx's Theory Of Value Explains The Business Cycle And Need For Crises:

No Alternative Exists 150 Years Later

Marx had an integrated value theory that explained how the so-called business-cycle operated, including in his own day. The perfected labour value theory requires a money commodity to make it work. This is not a "nice to have" part of the theory. It is essential to making it work. Marx's perfected theory also allows us to disprove and reject the three fundamental pillars of all bourgeois economic theory.

Modern neoclassical economics is based on the trinity of Say's Law, the quantity theory of money and the law of comparative advantage. This trinity is found in Ricardo as well. While Marx inherited and greatly deepened the Ricardian labour-based theory of value, neoclassical economics took over the Ricardian trinity rejected by Marx while discarding the Ricardian labour-based theory of value.

Say's Law of Markets was developed in 1803 by the French classical economist and journalist, Jean-Baptiste Say. Say was influential because his theories address how a society creates wealth and the nature of economic activity. To have the means to buy, a buyer must first have sold something, Say reasoned. So, the source of demand is prior to the production and sale of goods for money, not money itself. In other words, a person's ability to demand goods or services from others is predicated on the income produced by that person's own past acts of production.

Say's Law ran counter to the mercantilist view that money is the source of wealth. Under Say's Law, money functions solely as a medium to exchange the value of previously produced goods for new goods as they are produced and brought to market, which by their sale then, in turn, produce money income that fuels demand to subsequently purchase other goods in an ongoing process of production and indirect exchange. To Say, money was simply a means to transfer real economic goods, not an end in itself.

Under Say's Law, there can be no "overproduction" crisis because production creates its own demand. Marx dismissed this theory as that of a "trivial thinker". Commodities don't create their own demand. Exchange can be interrupted by any number of factors. Say's Law can be undermined by money hoarding, for example, when an interruption or delay in the circulation of commodities drags aggregate demand below aggregate supply; but if the money hoard consists of a produced commodity, which for Marx is gold, then hoarding can be considered to be just one form of commodity demand. The history of capitalism is proof that Marx was correct.

The Quantity Theory of Money, supported by Ricardo, argues that prices and wages are directly commensurable to the ratio of the number of commodities on one side and the quantity of money on the other in circulation. If the quantity of money in circulation halved, prices and wages would halve. This theory is needed for the operation of free trade.

Ricardo argued that if a country ran a deficit, money would flow out, prices would decline, and therefore become more competitive internationally, and so would eliminate the trade deficit. To produce this result, Ricardo argued that in national markets, absolute advantage prevails, but in international markets, comparative advantage operates. But that notion is also disproved as it is obvious today that the world market determines prices.

Marx used the crises in the UK in the mid-19th Century to prove that Ricardo's theory did not work in practice. When money (in this case gold) flowed out of the UK when it ran a trade deficit, prices did not decline. What happened was that interest rates rose and forced the economy into a recession to restore balance. Bourgeois economists view interest as simply the reward that capital receives for holding money. Marx saw interest as being governed by the supply and demand for gold.

That is why central banks, in the last analysis, can't control interest rates; the market does. It is inevitable that as the business cycle peaks, the demand for money capital peaks, and interest rates will rise and choke off the recovery. As the crisis deepens, money capital is accumulated and becomes more abundant, and interest rates decline, restoring the profit of enterprise and the desire to invest and produce more goods.

If the monetary authority allows the token money to depreciate as shown by a rising “price” of gold, the money capitalists will defend themselves by demanding a higher rate of interest. And they have the power to collectively enforce their will. This collective money power is greater than the powers of the central banks. This rise and fall in interest rates are part of the proof that gold remains the money commodity.

Only Working Class Can Overthrow System

Marx did, of course, have a quantity theory of money when it came to token money. But if token money is halved, prices double, the opposite of what Ricardo predicted. In the history of capitalism, who has been proved correct? Have trade balances been restored by free trade? Has the business cycle been eliminated? Has the gold price plummeted because of the reduction in demand? Post-Ricardo, bourgeois economists adopted marginalism as an economic theory. Marginalism argues that free-market capitalism would tend towards zero growth. Has that happened anywhere not subject to brutal US sanctions or war?

Marx predicted capitalism would be a system of expanded reproduction, and continual overall growth but with repeated crises. Has that happened? He predicted it would conquer and transform the globe in its image. Has that happened? He predicted there would be concentration and centralisation of capital. Has that happened? We should be super proud of the old man. No one has surpassed his insight into how the system works, why it must be overthrown, and why the working class is and remain the only class that can do that.

Non-Members:It takes a lot

of work to compile and write the material presented on these pages - if

you value the information, please send a donation to the address below to

help us continue the work.

Foreign Control Watchdog, P O Box 2258, Christchurch, New Zealand/Aotearoa.

Email